Founders and executives often perceive equity crowdfunding as a very expensive means of raising capital, making it a secondary or last-resort form of financing. Unfortunately, these people are not looking at the bigger picture–they are not thinking about dilution.

In order to help issuers better assess the opportunity to raise capital using equity crowdfunding, we created a simple model that looks at the tradeoffs between “cost of capital” and dilution across the three common types of equity financings: venture capital, banked or brokered raises, and equity crowdfunding.

You might find the results surprising: for the same net proceeds, a modest difference in the pre-money valuation could have an outsized effect on the dilution of early shareholders.

Ultimately, as a founder or executive of an early-stage company, you are taking a lot of risk, in addition to putting in a tremendous amount of effort. And it is your duty to protect the interest of yourself and other early investors.

In other words, it’s critical to carefully weigh the financing options available to your company to fund your growth plans, which in effect should make this tradeoff top of mind for any issuer considering raising capital.

But as with any decision, it’s not black and white. There are important aspects you should consider when reviewing the equity financing options available to you - read on below to learn more.

Setting The Table

It is important to note that the numbers we discuss are theoretical and intended to help issuers better understand the options available to them. It would not be possible to generalize the costs of capital and valuations without specifying the company, the market conditions, and virtually an infinite number of other factors.

But before we dive in further, we need to start with some definitions to align our understanding.

What is Dilution?

Generally, shareholder dilution refers to a decrease in the ownership stakes of existing shareholders as a result of a company issuing new shares. This can happen through a variety of means, such as stock issuances, stock splits, and acquisitions.

When a company issues new shares of stock, it increases the total number of outstanding shares, which can lead to a decrease in the value of each individual share. This can result in a dilution of the ownership stakes of existing shareholders, as they now own a smaller percentage of the company.

Dilution is a broad term, so for the examples discussed in this article, “dilution” refers to the total amount of equity the company must sell to raise a fixed amount of net proceeds relative to the final valuation of the company.

Put another way, due to the differing costs of capital, the total dollar amount raised for the same net proceeds to the company will differ. However, in the end, issuers should want to give up the smallest percentage of their company possible while still securing the necessary growth capital (in our example $5M of growth capital).

What is Cost of Capital?

In equity crowdfunding, the term “cost of capital” is often used to describe the actual amount paid to raise capital. It’s important to note that this definition is different from the classic definition you may have learned in your finance class.

In the traditional sense, "cost of capital" refers to the required rate of return that investors expect to receive for providing capital to a company, also known as the hurdle rate. This rate is based on the level of risk associated with the investment and the current market conditions, where higher risk opportunities or tougher market conditions result in higher rates.

For the purposes of this discussion, we are going to refer to “cost of capital” in the literal crowdfunding sense - the cost an issuer pays to complete a specific equity crowdfunding campaign.

Now that we are on the same page, let’s look at the options that might be available to an issuer (if they’re lucky!).

Venture Capital

Receiving VC funding can be a badge of honor - and based on what founders like to put in their LinkedIn tagline - we mean this in a literal sense.

There is almost certainly a cache that comes with being a “VC-backed” venture. Not to mention there can be benefits to being part of a broader network. On top of that, raising VC funding can be a time-efficient approach to raising capital (although far from a guarantee).

However, while VCs want to see incredible potential, they certainly don’t want to pay for it. Typically, founders will hit the street with a valuation in mind, and then be beaten down on valuation until they are left with an incredibly small piece of the pie.

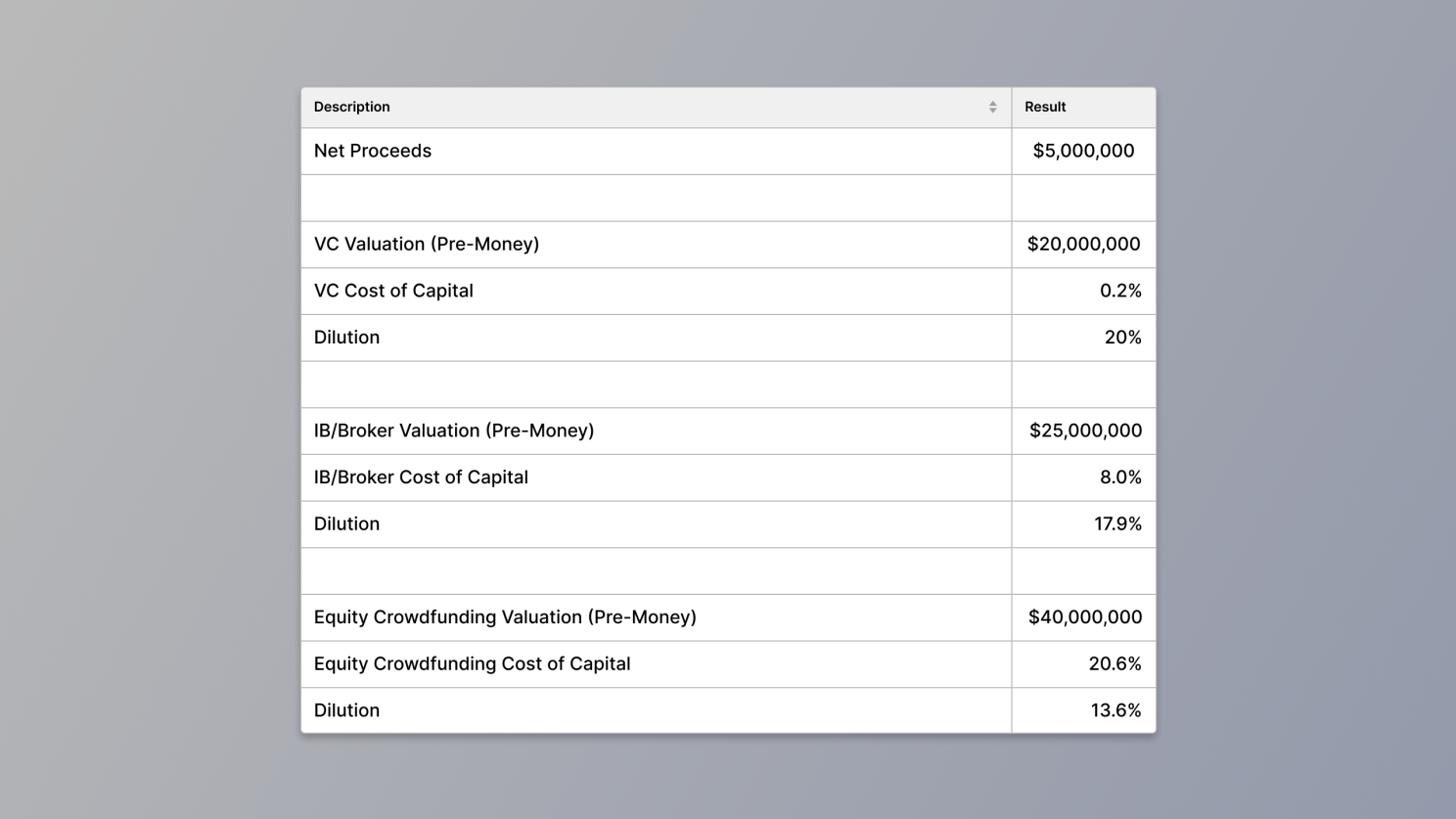

As shown by the example above, valuation at an early stage can have an outsized effect on the amount of the company given up by the founders.

On top of the valuation beat-down is the creation of SAFEs, where founders (and even other VCs) have an exceptionally difficult time piecing together how much of their company they will be giving away for different scenarios in the future (especially once SAFEs are stacked on top of each other).

The ultimate irony in this scenario is that VCs want founders and executives to “have skin in the game,” yet some squeeze so aggressively that it is no longer the case.

With that said, one clear advantage is that VCs like to see ALL of their funds go to the startup. So while there are some legal fees and costs for marketing collateral or roadshows or meetings, it is normally very low. For the purposes of this discussion, we have assumed a "cost" of around 0.2% of the raise.

Banked or Brokered Raises

Turning to banked or brokered raises, the experience differs. The cost is certainly higher, but the workload and timelines can be more in the company’s favor. However, the issue becomes a game of cat and mouse or at least a false sense of control regarding the valuation.

Bankers and brokers will often promise that the desired valuation can be achieved - “no problem, our network is loving the sound of the deal.” But when push comes to shove, the valuation comes under pressure, or more conveniently, there are sweetener warrants added that serve as an overhang for your cap table for years to come.

On top of this, the company ultimately isn’t the true holder of the relationship with investors. These are, after all, investors in the bank’s or broker’s network. And lastly, this approach only works if you are well-connected with the right people, which most new founders, unfortunately, are not.

The cost with a banked or brokered raise tends to be higher compared to raising from VCs, but they can also help push a slightly higher valuation to their network.

At face value, these firms typically charge around 7% cash and 7% warrant coverage, varying based on the quality of the company as well as the size of the raise. On top of these standard fees are often legal fees, roadshow costs, and advisory fees, among others. For simplicity, we have assumed a cost of 8% for our theoretical raise.

Equity Crowdfunding

In equity crowdfunding, the company and its executives quite literally set the terms of the raise through a filing with the SEC. They can also choose to add warrant sweeteners, perks, or other incentives to encourage large ticket investments.

As referenced previously, this type of raise can be costly, with fees from broker-dealers and platforms, as well as marketing agencies to fill your funnel. It can also be extremely time-intensive and, depending on the raise, there can be some upfront fees as well (legal, onboarding fees, marketing, etc.).

However, apart from setting your terms, there are some other benefits worth highlighting. The biggest is the opportunity to turn customers into investors and build a true community around your company. In the industry, people are starting to use the term “community round” more and more often.

Overall, equity crowdfunding is the most expensive form of capital. While the costs can vary substantially, we usually see a cost of capital in the range of 15-20%, with the wide variance driven by the quality of the issuer, different marketing strategies, and any existing customer base that can be marketed to at a low cost.

So how should you think about it?

Assuming all three options are available to you, what is the best strategy for you and your shareholders at the time you are making the decision?

As we showed above, for fixed net proceeds received by an issuer, the results were not what you might expect if you factor in the control an issuer has over the valuation.

Despite a cost of capital that is literally orders of magnitude higher, due to a higher valuation (2X), “pre-money” shareholders can experience up to 50% higher dilution (post-money) going a VC route over equity crowdfunding.

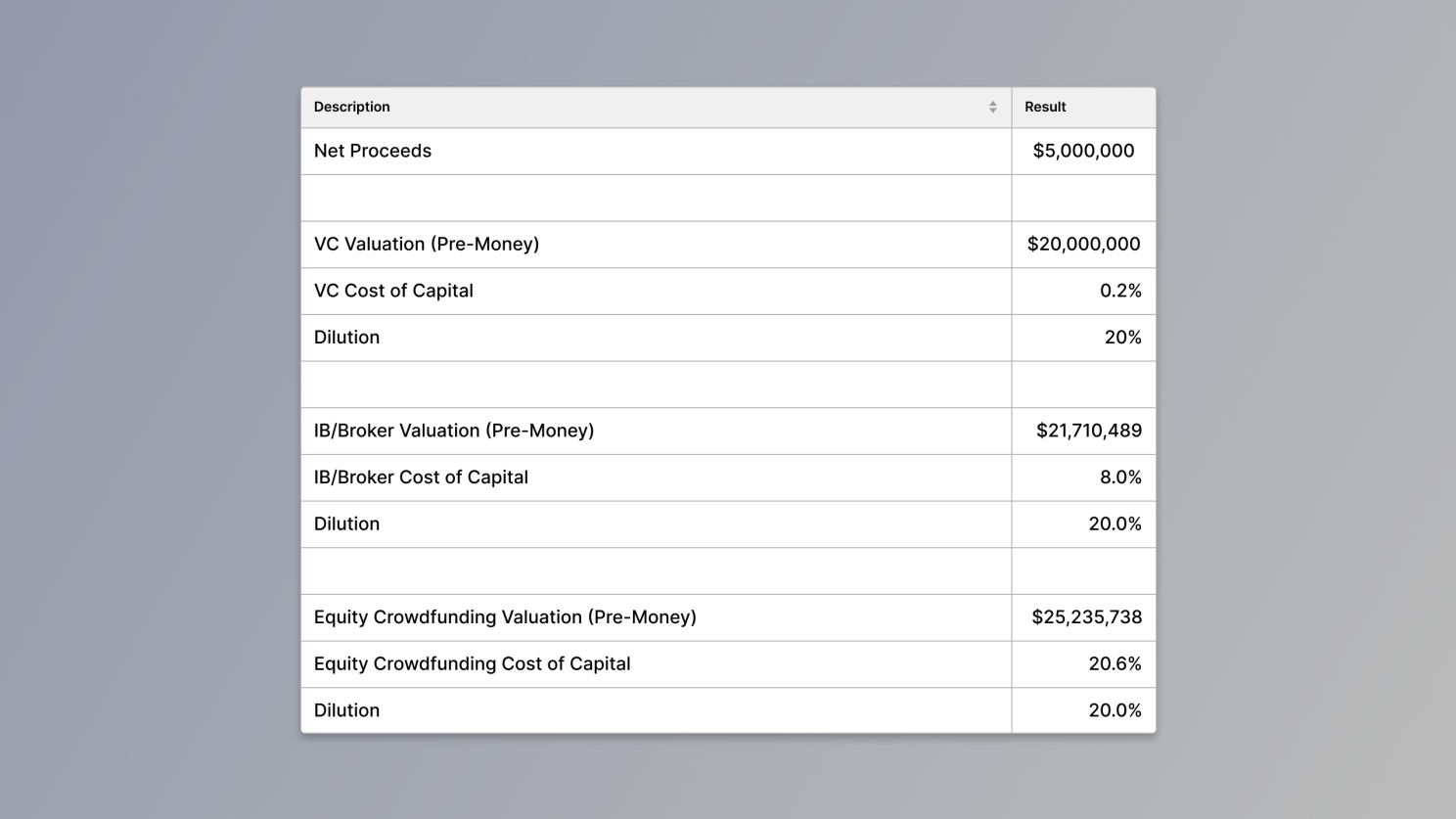

It’s important to note that the difference in valuation does not need to be extreme or even 2X for the dilution factor to be important. The below table outlines the “breakeven” valuations for equal dilution across the financing types.

It is important to note that we are adamantly against an issuer using equity crowdfunding to opportunistically increase the valuation beyond reasonable levels for retail investors. Further, we believe it constitutes fraud to mislead new investors with plans you know you cannot achieve but are promising or promoting regardless.

This also does not mean that the valuations obtained from VCs or bankers/brokers are necessarily fair either. Often, founders feel trapped into taking capital as they believe it’s the only way to fund their business, so they accept a highly dilutive deal.

In the end, founders risk it all to start their own businesses and they deserve to be compensated for this risk.